Global Macro Weekly Playbook (30 Jan)

Beware of the S&P 500 bullish trendline breakout & Powell may slap markets with a reality check

Greetings folks! Welcome to the latest edition of the “Global Macro Weekly Playbook” newsletter; where it will be a pivotal and jammed packed week with key economic events and data releases; FOMC, ECB, and BoE monetary policy decision outcomes coupled with US non-farm payrolls, US ISM manufacturing & non-manufacturing PMIs, as well as China manufacturing PMI for January will be closely watched after the sudden reversal of strict zero-Covid policies in early December.

Also, the US earnings season is still in the limelight where market participants will have further insights into the odds of a looming earnings recession for corporate America where the rest of the Big Tech (Meta Platforms, Alphabet, Amazon, and Apple) will report this week together with other major firms such as AMD, Qualcomm, and Caterpillar.

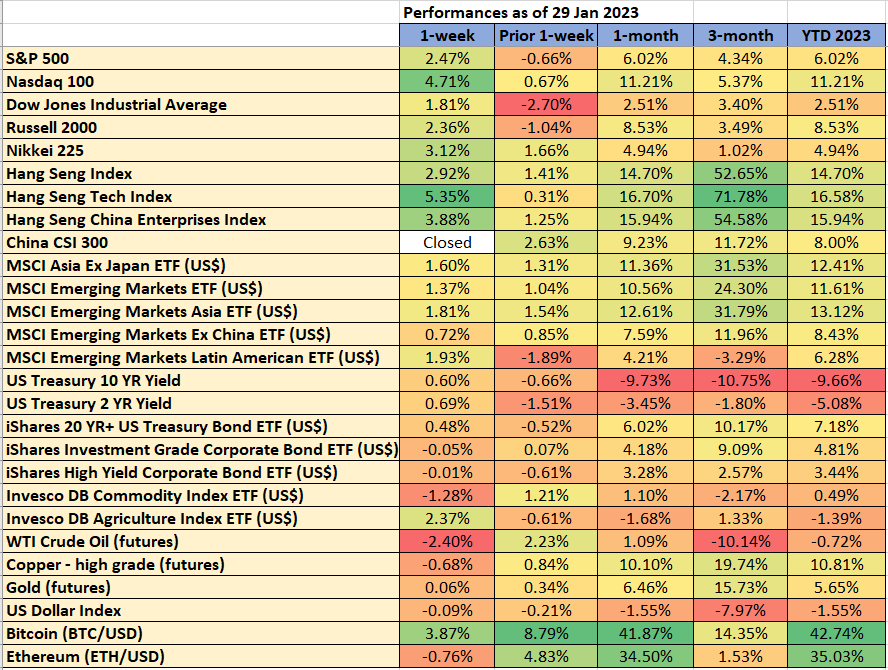

Recap for last week…

Data from TradingView & MarketWatch

The same “risk-on” narrative in the equities space has been built primarily on the hope of a Fed Pivot and a transition to a start of an interest rate cut cycle to begin in the latter part of 2023.

The S&P 500 has managed to stage a clear bullish breakout above the “most-watched” trendline resistance in place its current all-time level of 4,818 printed on 4 January 2022. It is en routing to record a monthly gain of 5.32% and the technology and growth-heavy Nasdaq 100 is shining better with a monthly gain of 9.59%, its best monthly return since July 2022. (PS: I am skeptical about the S&P 500 bullish breakout; will offer more insights in the next portion).

In my prior week’s newsletter, I highlighted the bullish setup in the US 10-year Treasury yield that is likely to put a halt to the “risk-on” behavior (click here for a recap) and last week’s price actions on Gold, WTI Crude and Copper have started to show signs of upside momentum exhaustion. Hence, Intermarket analysis from these asset classes can be the canary in the coal mine to indicate a potential bearish reversal (at least a multi-week one) for global equities in general.

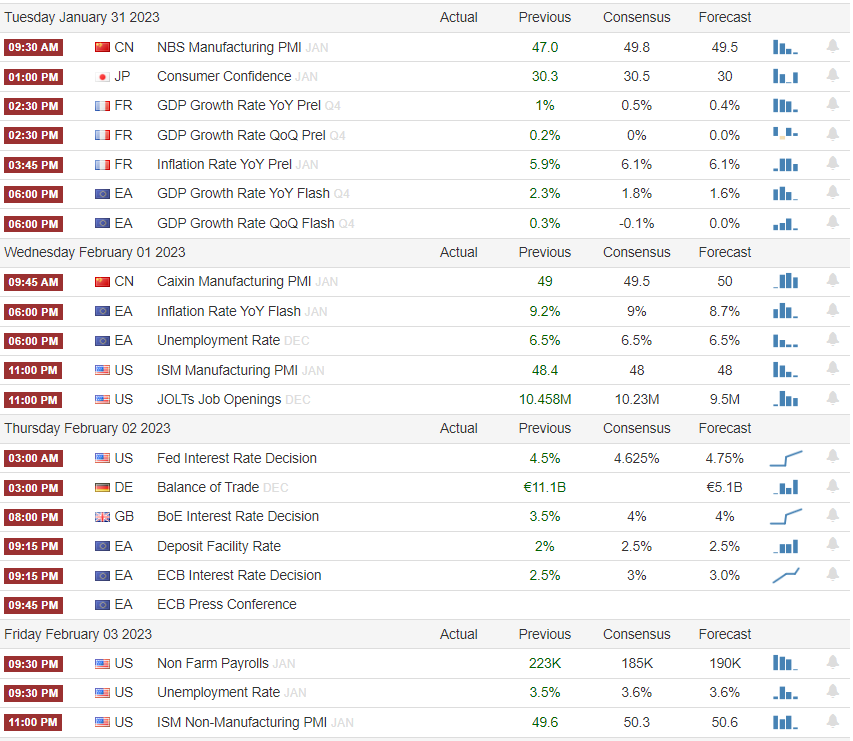

Key economic data & events to watch for this week

Source: Trading Economics (SG timing)

US Q4 2022 earnings season: US Big Tech galore; Meta Platforms will report its numbers on Wednesday after the close followed by Amazon, Apple, and Alphabet/Google after the close on Thursday. Other notable firms to watch out; Exxon Mobile, UPS, AMD, Amgen, Caterpillar, and Electronic Arts. A full table of details as below;

Source: Earnings Whispers

Going forward...

Fed Chairman Powell’s maestro in providing more “transparent” guidance on Fed’s monetary policy and its framework in public has been challenged by market participants in the financial markets.

In the recent three Fed FOMC meetings, Powell and company have reiterated that restrictive and higher interest rates are to stay throughout 2023 and at best, the first rate cut to come in 2024. In contrast, markets have started to bet that the Fed is wrong at this key “turning point” of the economy where the recent data on US CPI and PCE price indices suggested that inflationary pressures have peaked and economic damage from the current rate hike cycle has started to be detrimental towards the economic growth as seen via the recent layoffs announcements by US Big Tech firms that came in like a “falling dominos-styled” effect.

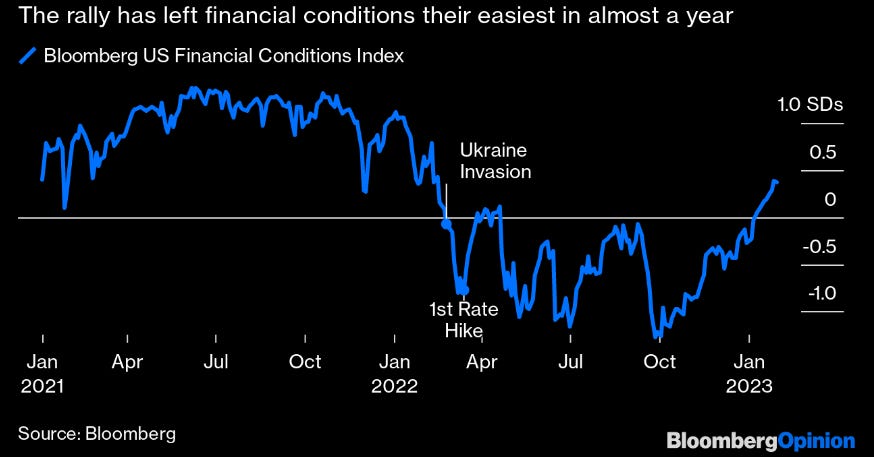

The markets have priced in a Fed Pivot and they will be “forced” to cut by 50 bps by the end of 2023 which has triggered the recent “risk-on” rally that saw the S&P 500 record a gain of 16.6% from its October 2022 low. Apart from using interest rate hikes to cool down inflationary pressure, central bankers like the Fed also target other variables such as financial conditions that are derived from the movements of asset prices and market participants’ aggregate behavior in the financial markets and most importantly, the financial markets have become more interlinked with the real economy since 2000.

This is how a simple financial markets-based mechanism works its way to the real economy, the Fed embarks on a tightening monetary policy guidance & path to slow the economy=>equity valuations fall + longer-term bond yields increase=>financial conditions tighten=>consumers and corporations spend and invest lesser=>inflationary pressures fall.

Right now, the reverse process is taking shape where equity valuations have started to inch higher coupled with a decrease in bond yields from their recent peak in their Oct 2022. The Bloomberg US Financial Conditions Index is now looser in the months before the first Fed funds rate hike on 17 March 2022.

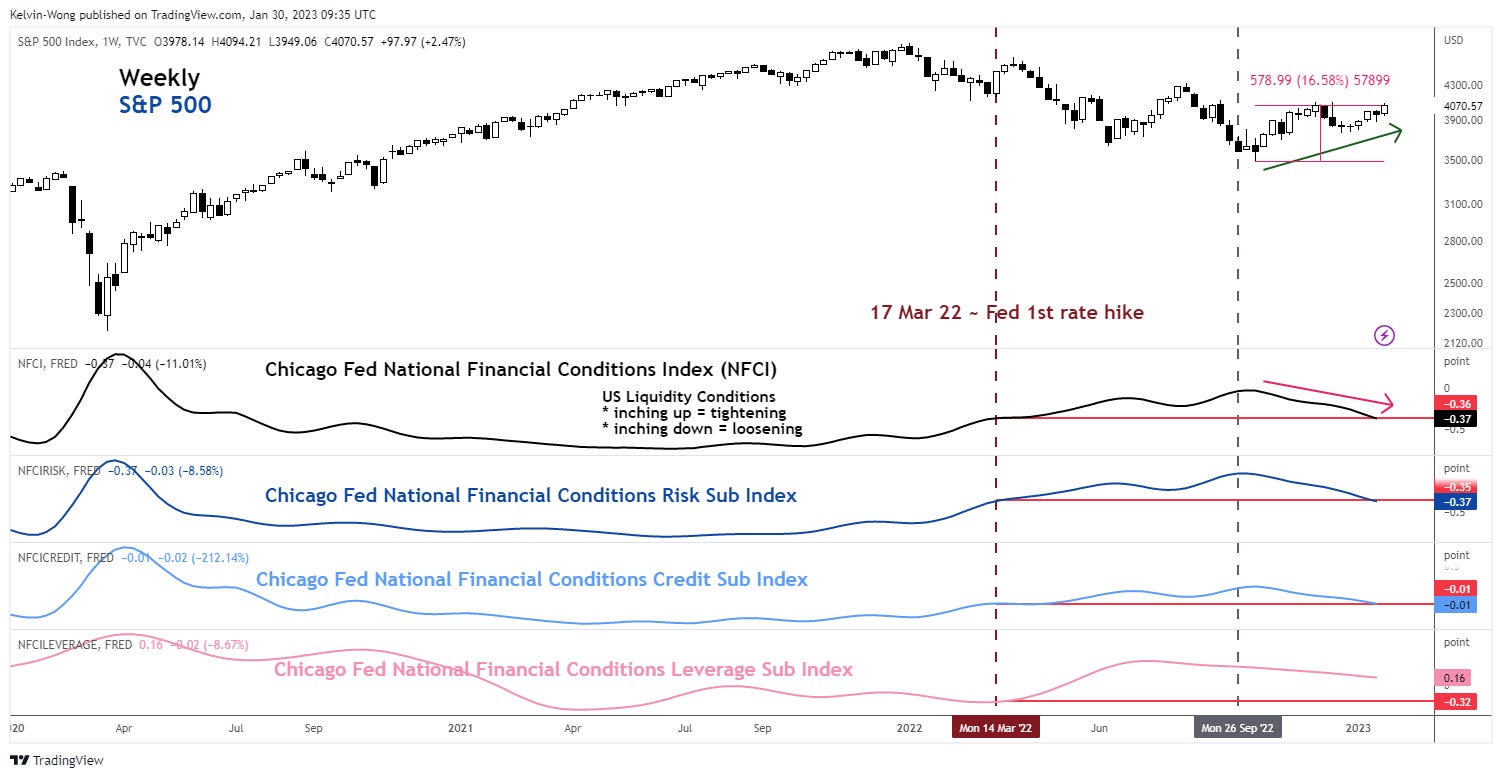

A more comprehensive measure of financial conditions, the Chicago Fed National Financial Conditions Index (NCFI) takes into account the movements seen in money markets, debt and equity markets have dipped to -0.37 based on its latest data for the week ended 20 January 2023, below the level of -0.36 printed on the week after the first Fed rate hike on 17 March 2022. Interestingly, the current state of loosening condition in the NCFI has coincided with the recent short-term uptrend in the S&P 500 from its Oct 2022 low of 3,491.

Source: TradingView as of 30 Jan 2023

If financial conditions continue to loosen further, it will translate into higher inflationary pressure in the months ahead (as there tends to be a lag between the real economy and the movements depicted in financial markets) which indicates an indirect “slap” in Powell’s face given by market participants in the financial markets.

Hence, can Powell and company tolerate the intensity of such a “slap”? I guess Powell will likely use the press conference (no “dot plot” projections for this upcoming FOMC) to guide (“slap-backed”) market participants to reality this week.

Beware of the recent bullish trendline breakout of the S&P 500

The S&P has staged a clear bullish breakout from its trendline that has been in place since its current all-time high of 4,818 printed in January 2022 with a weekly close above it and a gain of 2.3% above the trendline; a positive feat.

I have decided to examine previous similar bullish trendlines breakout with two prior conditions in place; (1) the S&P 500 hit a fresh all-time high before it declined & (2) the decline must have at least a 20% drawdown from its all-time high before the bullish trendline breakout. I ignored steep declines such as the pandemic-induced waterfall slide of January to March 2020 where graphical trendlines analysis is futile at such a juncture.

Since 1970, there were seven such occurrences; September 1970, October 1982, October 1998, May 2001, May 2008, January 2019, and January 2023.

Bullish breakouts that led to new all-time highs were the periods of September 1970, October 1982, October 1998, and January 2019 where these breakouts had been accompanied by increasing volume.

On the other hand, the resistance trendline breakouts of May 2001 and May 2018 failed and led to lower lows thereafter and these bullish breakouts have been accompanied by lackluster volume readings.

Right now, last week’s bullish breakout has been accompanied by lackluster volume reading which causes me to be cautious, perhaps a “fake head” in the making?

US Sectors Relative Strength – Prior leadership group is weakening

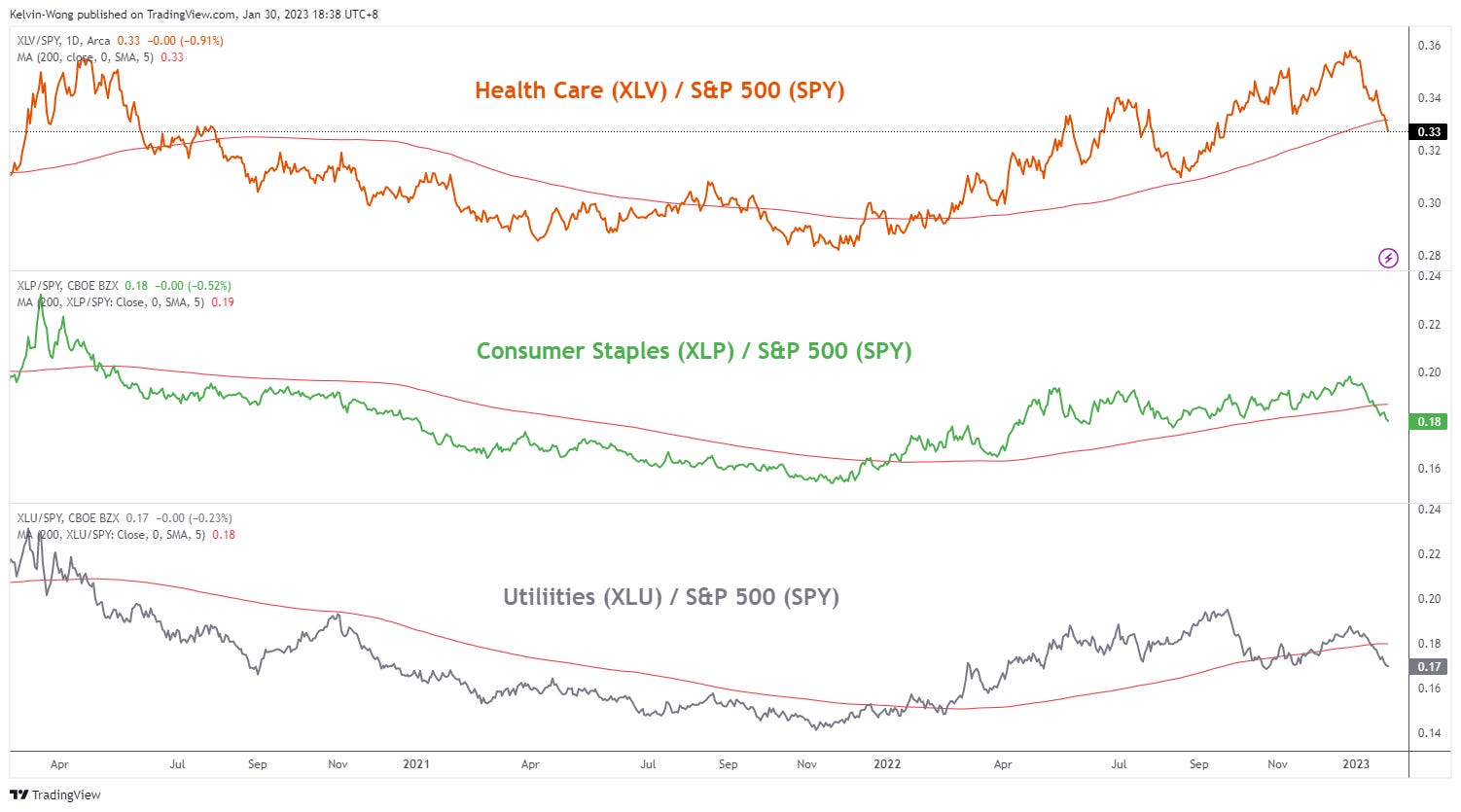

Despite the recent major bearish trend of the S&P 500 that has taken form from its January 2022 all-time high of 4,818 to its October 2022 low of 3,491, the defensive sectors (Health Care, Consumer Staples & Utilities) took a leadership role during this period; outperformed the S&P 500 and even made new 52-week highs (Health Care & Consumer Staples in April 2022, Utilities in September 2022).

But in recent weeks, their relative strength (as a ratio against the S&P 500) has declined and their ratios have broken below their respective 200-day moving averages for the first time in eleven months.

Source: TradingView as of 30 Jan 2023

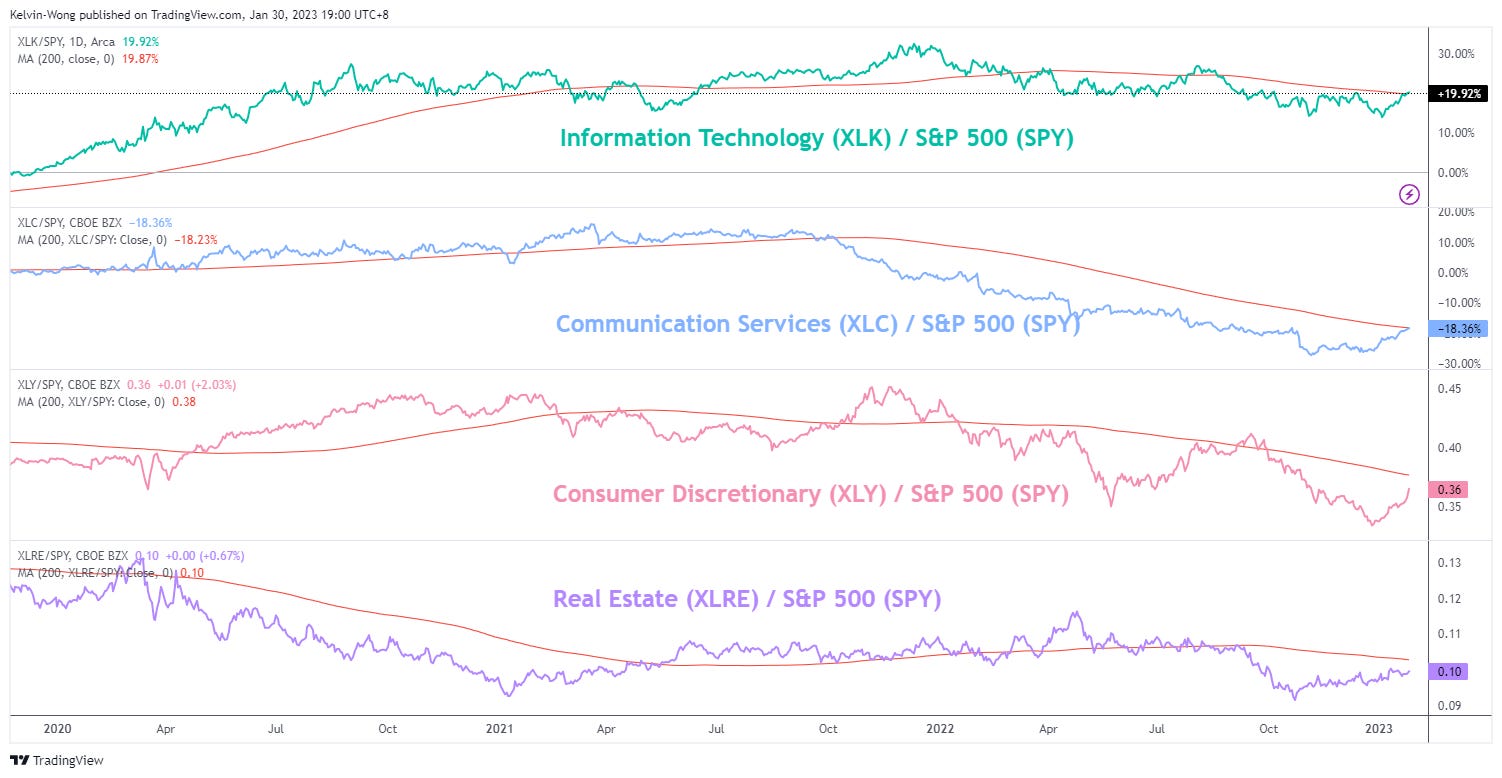

On the other hand, the beaten down and prior underperforming sectors (Information Technology, Communications Services, Consumer Discretionary, and Real Estate) have outperformed in the recent four weeks as indicated by an improvement in their relative strength conditions but their ratios are still below their respective 200-day moving averages.

Source: TradingView as of 30 Jan 2023

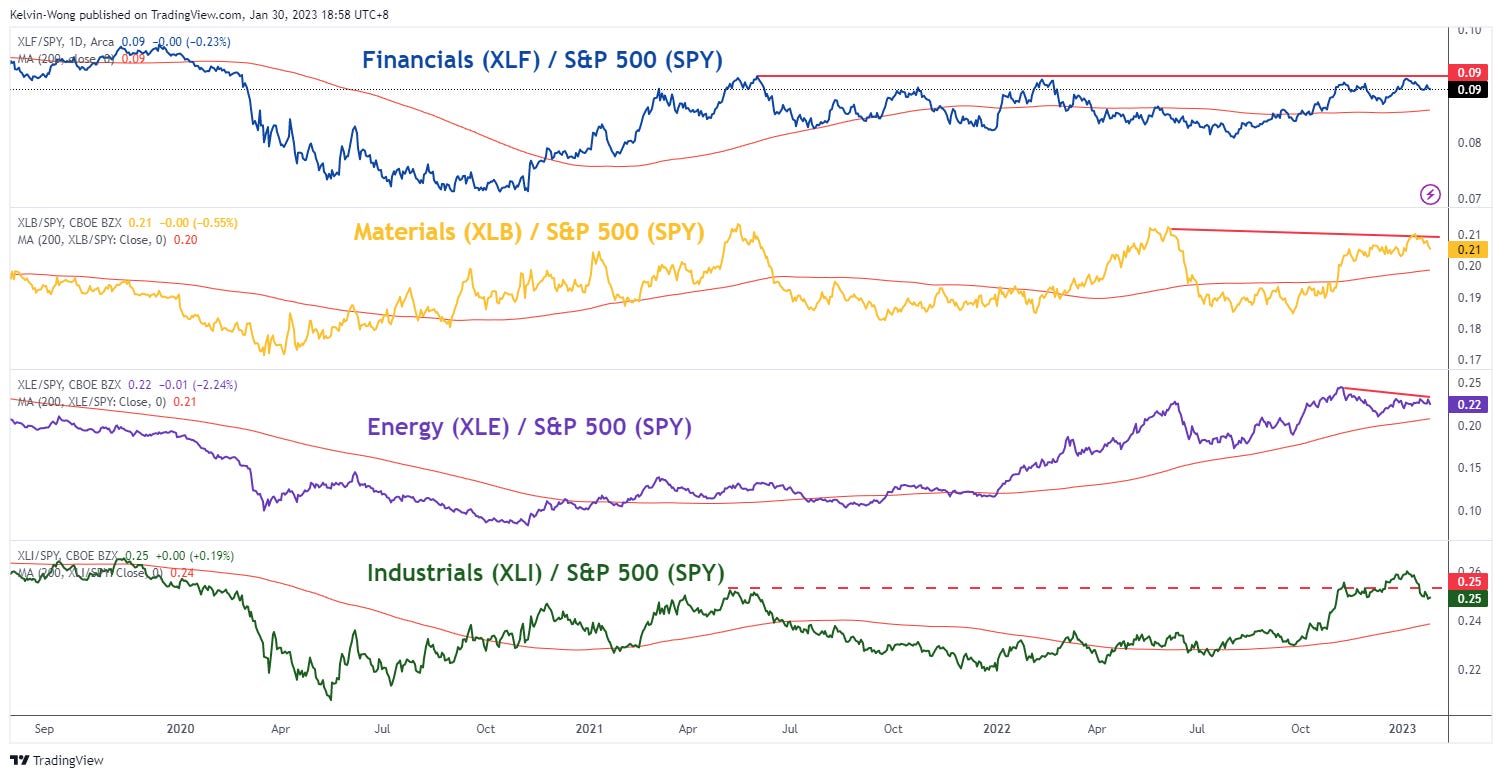

The ratios of the other sectors; Financials, Materials, Energy, and Industrials are still holding above their respective 200-day moving averages; but their ratios are not printing “higher highs” which indicates headwinds for their relative strength conditions.

Source: TradingView as of 30 Jan 2023

Hence, a relative strength analysis across the 11 US sectors does not seem to justify a “wholesome” rally under the hood but rather a FOMO-induced rally and short-covering activities on the prior worse beaten down sectors; Information Technology, Communication Services, and Consumer Discretionary.

Global Macro Charts Of The Week – curated based on integrated technical analysis (fractals, momentum & graphical)

New additions…

EUR/CHF – Medium-term corrective rebound phase remains intact

Source: TradingView as of 30 Jan 2023

Since its 26 September 2022 low of 0.9403, the EUR/CHF cross rate has been evolving within an ascending channel supported by the narrative of an increasingly hawkish monetary policy guidance by the ECB over its Swiss counterpart, SNB where inflationary pressure in Switzerland is less than a third of the pace versus the Eurozone area.

Watch the 0.9935 key medium-term pivotal support (also confluences with the 200-day MA) for further potential push-up towards the next resistance at 1.0223 with a maximum limit set at 1.0320 (the upper boundary of the ascending channel & Fibonacci extension cluster). On the flip side, a break with a 4-hour close below 0.9935 jeopardizes the bullish tone for a slide toward the next support at 0.9755.

Gold (Spot US$/OZ) – Bullish exhaustion signals detected, at risk of a multi-week correction

Source: TradingView as of 30 Jan 2023

The 21% rally from its September 2022 low of 1,614 has almost reached a key medium-term inflection level of 1,957 coupled with a continuous bearish divergence signal being flashed out by the 4-hour RSI oscillator since 16 January 2023. These observations suggest that the 3-month plus medium-term uptrend phase from September 2022 is likely to have reached a terminal/exhaustion point where the odds have increased at this juncture to kickstart a multi-week corrective decline.

Watch the 1,957 key medium-term pivotal resistance for a potential decline towards the next supports at 1,865 and 1,825. On the other hand, a 4-hour close above 1,957 put the bears on hold for a squeeze up toward the next resistance zone of 1,980/2,000.

Short-term Tactical Global Macro Model Portfolio

Below is a summary table of assets from prior newsletters’ “Global Macro Charts Of The Week”

Source: TradingView as of 30 Jan 2023

Disclaimer

The content of this newsletter should not be construed as a solicitation to invest and/or trade. This is not trading/investment advice and all content is portrayed as opinion. Past performance is not indicative of future performance.

That’s all for today. I hope you enjoyed my analysis; do feel free to forward it to friends, and colleagues, and remember to subscribe to the newsletter.