Global Macro Weekly Playbook (9 Jan)

The Fed against the market & China’s Big Tech outperformance

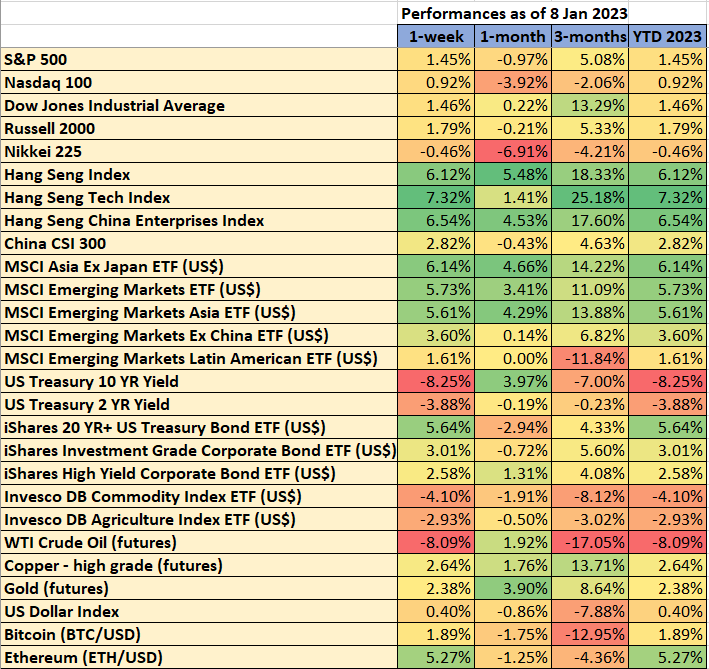

Recap for last week

Data from TradingView & MarketWatch

The first trading week of 2023 has kickstarted on a solid footing for risk-on-related assets, especially towards the later part of the week as traders embraced further optimism of growth reinvigoration out from China and December’s US labor market report (nonfarm payrolls) has indicated that wage growth grew by 0.3% y/y that came in slightly below consensus of 0.4%.

China-related (Hang Seng Index, Hang Seng TECH & Hang Seng China Enterprises) and Asian stock indices were the top performers with weekly gains of 6% to 7% while US stock indices struggled in the first half of last week and their weekly positive gains were only attributed by last Friday’s positive pop post nonfarm payrolls data release.

The slowdown in US wage growth has kind of triggered a “comforter” that the current hawkish guidance embarked on by the Fed is out of sync with reality where market participants have priced in a first Fed funds rate cut in Q3 2023 based on Fed funds rate futures pricing despite the latest Fed minutes from the December 2022 FOMC has reiterated that there is no pivot on its current tight monetary policy stance in the near future and a rate cut will not be appropriate in 2023.

Over to the China growth narrative where a change in tone of industry-related policies has taken over the positive vibes from the transition from zero-Covid to “reopening freedom”. Further concrete signs have taken shape that policymakers are likely to have ended close to two years plus of draconian measures on technology platform companies; Chinese regulators have given the nod to Ant Group, the fintech arm of Alibaba for a request on a capital expansion plan of 18.5 billion yuan from 8 billion yuan. Recalled that Ant Group’s business practices were the “tipping point” that triggered the industry-wide crackdown. Its mega IPO of US$37 billion was suspended abruptly in November 2020; thereafter more regulations and penalties were imposed on other China-based technology platform companies.

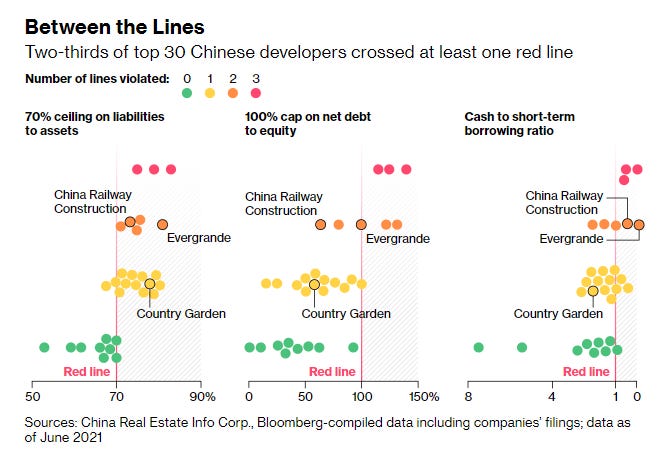

Also, regulators have started to indicate imminent plans to further relax restrictions on Chinese property developers’ borrowings and loosen the stringent “three red lines” policy on leverage usage that triggered a massive credit crunch on Evergrande, a major developer that morphed into one of the biggest real estate meltdowns in China’s history last year which has threatened to snowball into a significant systematic risk for the country’s financial system.

Gold has also benefited from the Fed funds rate cut narrative where it recorded an 8-month high and weekly gain of 2.38%, its third consecutive weekly positive return.

On the contrary, the impending Fed funds rate cut (to alleviate current economic downturn conditions in order to promote future growth) as implied by the current state of market participants’ transactions in the interest rate futures market and China’s growth reinvigoration narrative have not been translated to oil prices. WTI crude oil futures has continued its medium-term downtrend trajectory since 7 November 2022 and ended last week with a loss of -8.09%, its worst weekly performance since 5 December 2022.

Key economic data & events to watch for this week

10 January, Tuesday - Tokyo CPI (Dec); considered as a leading inflation indicator for nationwide Japan CPI that will be released one week later on 19 January. Consensus is set up for a further increase in both Tokyo CPI and Tokyo core CPI respectively; 3.9% y/y from 3.8% y/y (Nov) and 3.8% y/y from 3.6% y/y (Nov). If consensus turns out as expected for Tokyo’s core CPI, it will be the sixth consecutive month of increase above Bank of Japan’s 2% target. A further potential JPY strength cannot be ruled out as it may provide inertia for BOJ to adopt a more hawkish stance on its existing ultra-loose monetary policy after it has widened the band of its yield curve control program on the 10-year JGB yield in December.

12 January, Thursday - US CPI (Dec); estimates are indicating a further dip in inflation to 6.5% y/y from 7.1% y/y (Nov), and core inflation (ex-food & energy) is expected to slow down to 5.7% y/y from 6% y/y (Nov). Inflationary growth has started to inch lower every month since June 2022 red hot print of 9.1%y/y.

Last Friday’s rallies seen in the major US stock indices have been built on the “Fed Pivot” narrative (again) and a weaker US CPI print (below estimates) is likely to add further impetus for the bullish camp.

In a nutshell, I do think markets are still hyping that old playbook book narrative that any economic growth-related slowdown indicators are likely to prompt the Fed to unleash its liquidity tap and hench jumpstart another major impulsive uptrend phase for the US stock indices. The Fed has made it clear that its primary objective is to keep elevated inflation in check to prevent any form of reacceleration that occurred in the 1970s.

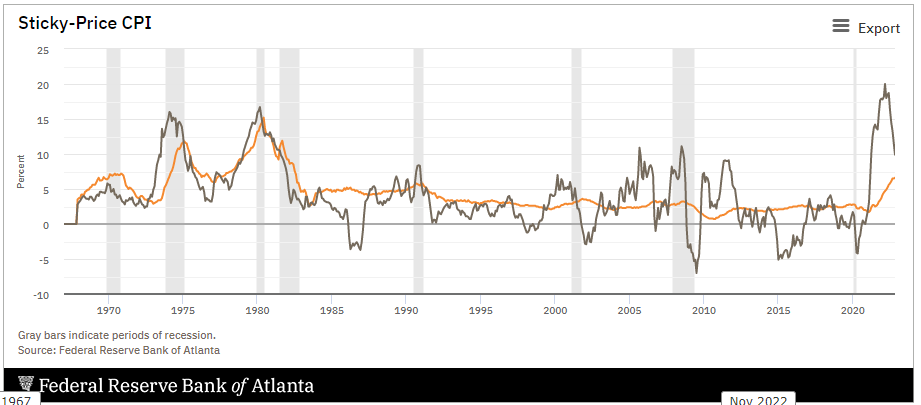

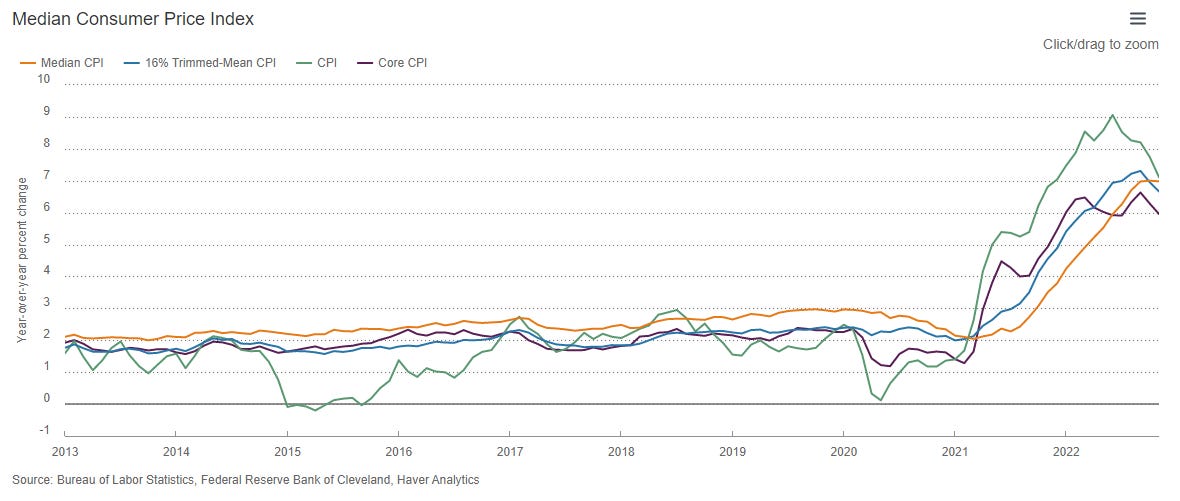

Also do take keep watch on median CPI (stripped out biggest outliers’ components) and sticky CPI (goods & services whose prices need to be set well in advance & are difficult to change quickly), both data will be released on the same day and remained elevated based on their respective previous prints.

Atlanta Fed Sticky-Price CPI has continued to increase; 6.6% y/y (Nov 22) vs 6.5% y/y (Oct 22)

Cleveland Fed Median CPI has not shown any signs of slowing down; remained unchanged at 7% y/y (Nov 22)

13 January, Friday - US Michigan Consumer Sentiment Flash (Jan); after it hit its all-time low of 50 level reading in June 2022, US consumer sentiment has improved marginally in the past few months with a print of 59.7 in December but it is still at its lowest level in a decade. Consensus is expecting a slight improvement to 60 on the backdrop of a further decline in inflationary expectations.

US Q4 2022 earnings session kickstarts; the major banks, Bank of America, Citigroup, Wells Fargo, JP Morgan, and BlackRock will report their respective earnings numbers on Friday, 13 January before the US market opens.

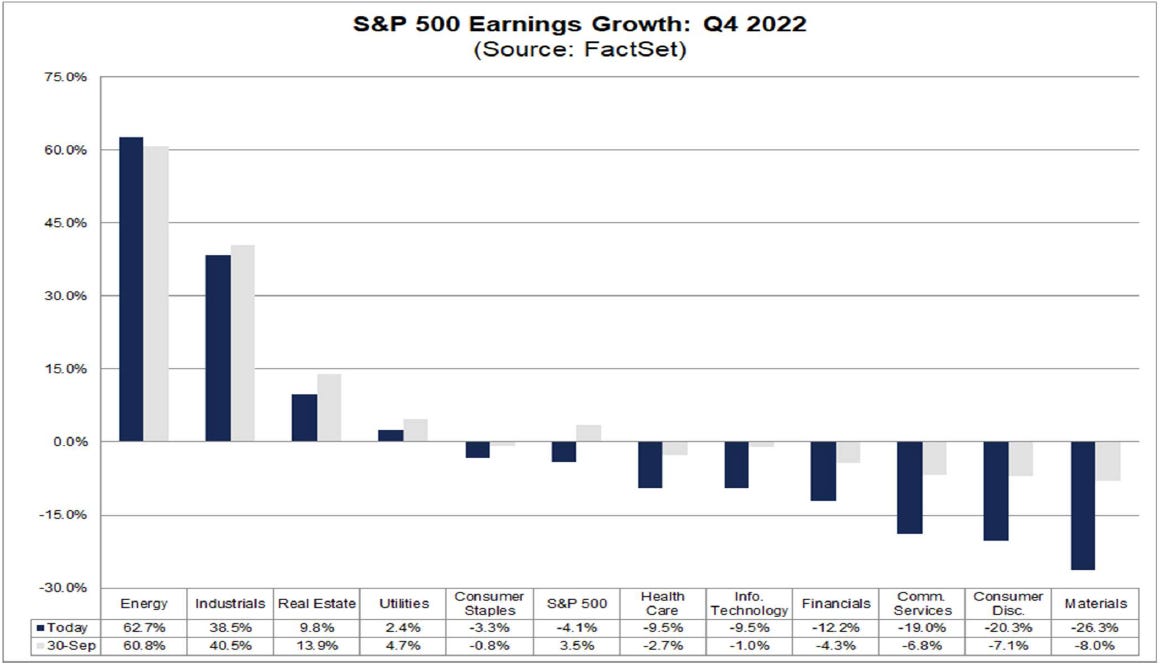

Data from FactSet as of 6 January 2023 has suggested that the Q4 2022 estimated earnings growth for the S&P 500 is expected to come in at a decline of -4.1% y/y and if it turns out as expected, it will be the first year-over-year earnings decline since Q3 2020 (-5.7%).

A notable observation is on the Financials sector where its Q4 2022 earnings expectations have deteriorated further to -12.2% y/y from -4.3% y/y recorded earlier on 30 September 2022 which also underperformed the S&P 500 Q4 2022 estimated earnings growth.

Source: FactSet as of 6 Jan 2023

Global Macro Charts Of The Week – curated based on integrated technical analysis (fractals, momentum & graphical)

Hang Seng TECH Index (futures) – Medium-term uptrend remains intact

Source: TradingView as of 9 Jan 2023

No clear signs of bullish exhaustion for its medium-term uptrend phase in place since the 24 October 2022 low of 2,649. Watch the 4,216 key medium-term pivotal support on the Hang Seng TECH Index (futures) for a potential continuation of its impulsive up move towards the next resistances at 4,820 and 5,180 before the risk of a multi-week correction occurs.

On the other hand, a break with a 4-hour close below 4,216 invalidates the bullish scenario to kickstart the multi-week correction process towards 3,873 support in the first step.

AUD/CAD – Bullish breakout trajectory remains intact

The AUD/CAD cross pair has continued to evolve in a medium-term bullish configuration since its 20 October 2022 low of 0.8598. Recent price actions have managed to retest and stage a bounce off its former major descending channel resistance last Friday, 6 January.

Intermarket analysis also supports a weaker CAD on a relative basis due to the bearish dynamics in play for oil prices. A further impulsive up move sequence for AUD/CAD cannot be ruled out towards the next resistance at 0.9500 as long as 0.9120 key medium-term pivotal support holds. However, a break with a 4-hour close below 0.9120 invalidates the bullish scenario for a slide toward the next support at 0.8890.

Disclaimer

The content of this newsletter should not be construed as a solicitation to invest and/or trade. This is not trading/investment advice and all content is portrayed as opinion. Past performance is not indicative of future performance.