Global Macro Weekly Playbook (28 Feb)

The China stimulus mirage

Greetings folks! Welcome to the latest edition of the “Global Macro Weekly Playbook” newsletter where we will be taking a deep dive into the common narratives to uncover macro mispricing and how it impacts the broad-based asset classes from a tactical perspective.

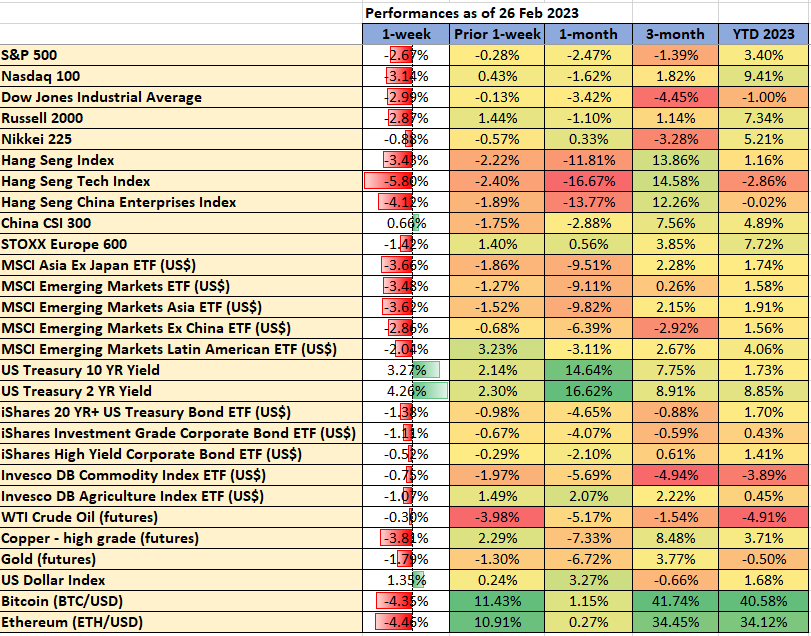

Recap for last week…

Data from TradingView & MarketWatch

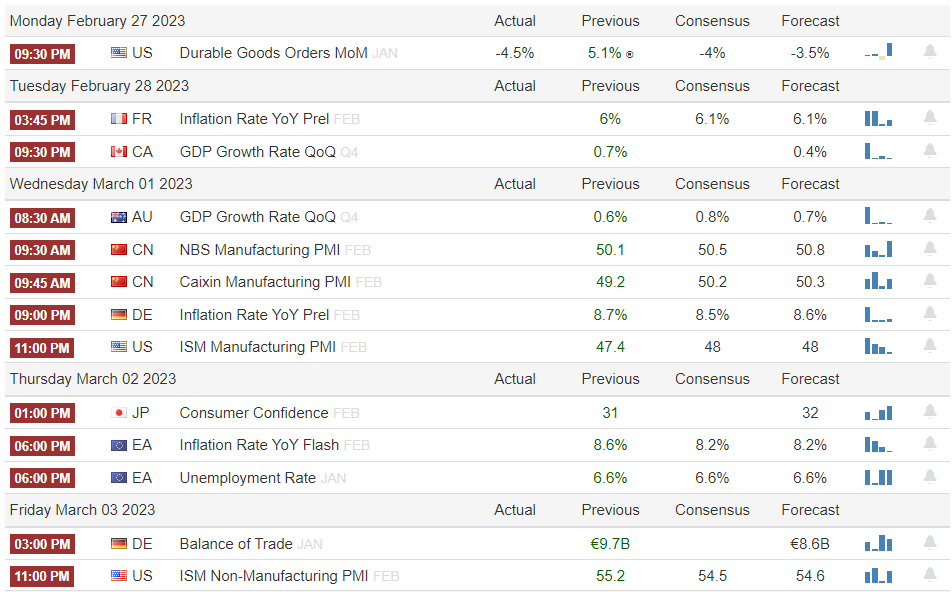

Key economic data & events to watch for this week

Source: Trading Economics (SG timing)

Other notable key economic data and events to watch:

US Conference Board Consumer Confidence (Feb) on Tuesday, 28 February, China Caixin Services PMI (Feb) on Friday, 3 March.

US Q4 2022 earnings season: the tail-end of earnings reporting in the US; key firms to watch for this week will be Zoom Video, Workday, Rivian, NIO, Salesforce, Target, Best Buy, Costco, and Broadcom. A full table of notable reporting firms is as follows;

Source: Earnings Whispers

Going forward...

The world’s second-largest economy, China is set up for a key political and economic annual event; the “Two Sessions” that kickstarts on Sunday, 5 March with the sitting of the National People’s Congress.

Outgoing Premier Li Keqiang is expected to deliver a government work report that includes growth targets for 2023 as well as fiscal budget and policy support for recovery from the prior two-year plus of draconian Zero-Covid measures, clampdowns on the “growth-oriented” business practices of internet platforms/digital gaming/China Big Tech firms as well as the liquidity crunch inherent in the property market that has a high risk of creating a systematic fallout in the entire Chinese economy.

Both the local Chinese stock market and global financial markets have already started to price in such expansionary policies to kickstart growth in China from a continuation of dovish guidance and liquidity support given by China’s policy-makers and state-related bodies since Q4 2022.

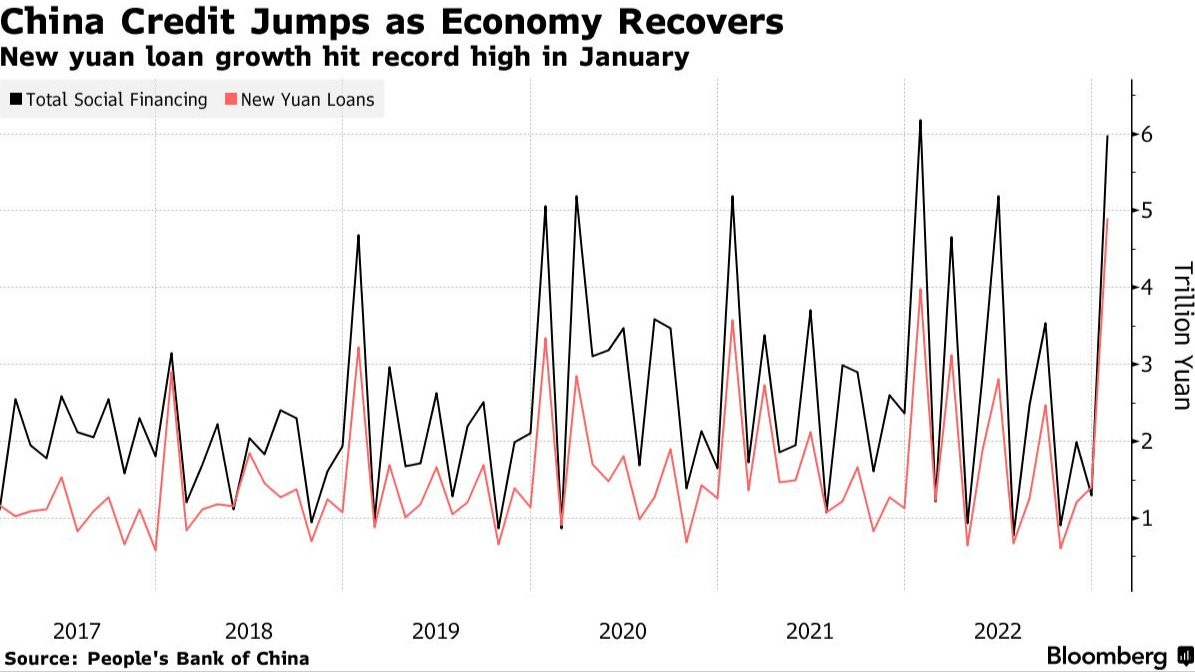

PBOC, China central bank & banking regulators advised Chinese banks to front-load credit expansion

Financial institutions in China offered a record amount of new loans in January 2023 that amounted to 4.9 trillion yuan, above a record of 3.98 trillion yuan a year ago, pushing the M2 measure of the money supply by +12.6% y/y, its fastest gain since April 2016.

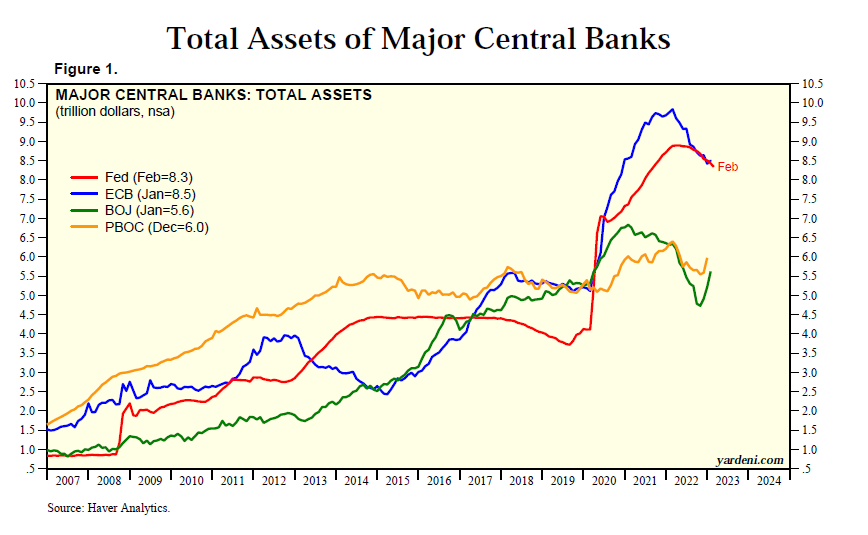

PBOC’s current liquidity pumping (together with BOJ) is offsetting partially the tightening stances from Fed & ECB

Source: Yardeni Research as of 25 Feb 2023

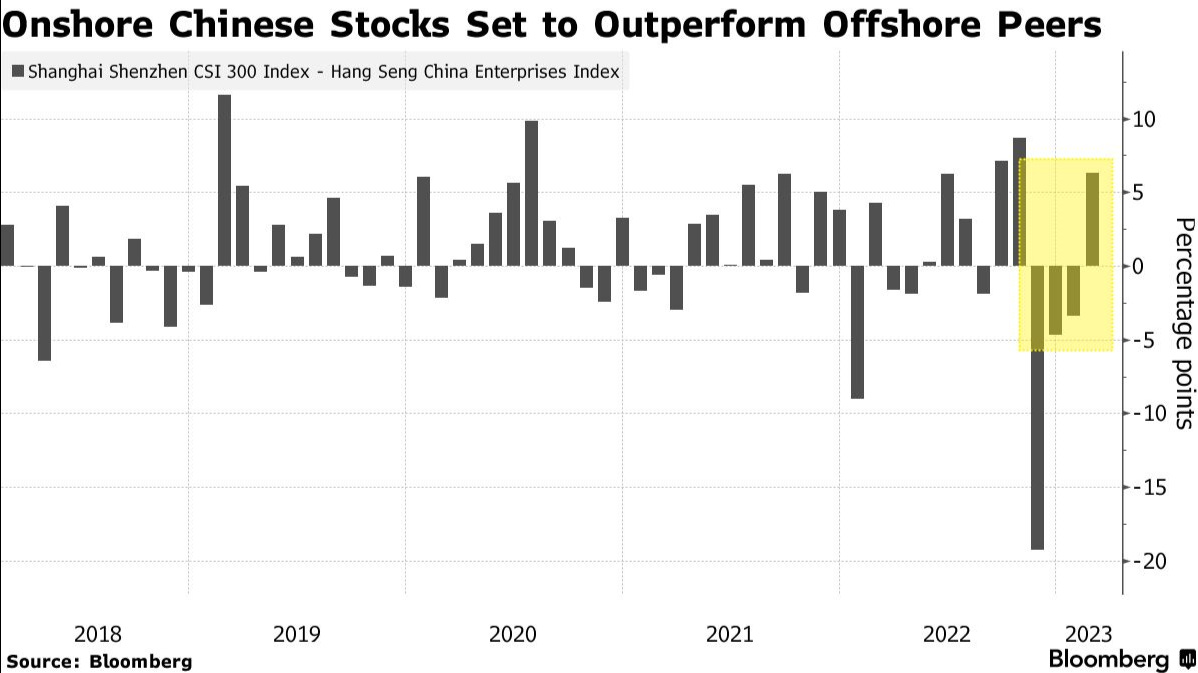

All in all, it has triggered a positive feedback loop in both “A” and “H” shares of Chinese corporations amid a slower pace from the “A” shares. The Hang Seng China Enterprises Index (offshore “H” shares barometer) rallied by 58% from late Oct 2022 to Jan 2023 whereas the CSI 300 Index (onshore “A” shares barometer) recorded a gain of only 22% over a similar period.

Other China-related stock indices such as the Hang Seng Index and the Hang Seng TECH Index (a barometer for China Big Tech also recorded stellar gains of 55% and 77% respectively which in turn triggered a positive feedback loop into global risk assets via a weakening of the USD (indirectly).

The recent optimism seen in China and its related stock markets has prompted most sell-side research houses of major investment banks to upgrade allocation recommendations towards Chinese equities due to relatively lower valuation versus the rest of the world and supportive domestic expansionary policies.

Most sell-side research is now favoring a bullish bias catch-up play for “A” shares to close the AH premium gap to take advantage of upcoming “Two Sessions” to be a fresh catalyst for China stock market where more potential stimulus measures targeting consumers and property sector are likely to be announced as China’s top leadership has emphasized boosting domestic demand as a top priority in 2023.

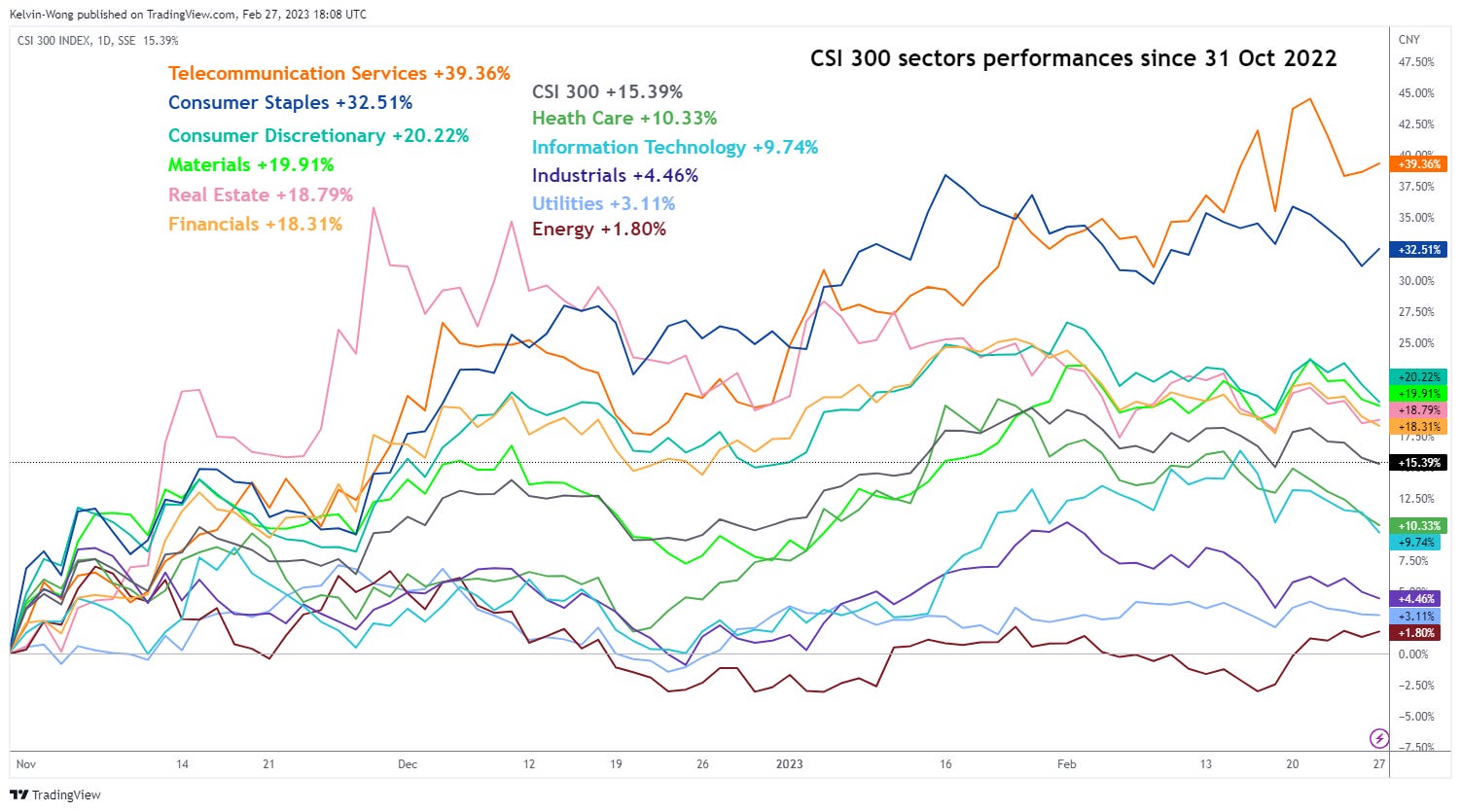

The story so far for onshore China “A” shares sectors

Source: TradingView as of 27 Feb 2023

All the 11 CSI 300 sectors are still posting positive gains since the start of the “expansionary induced policies’’ on 31 October 2022. So far, the outperformers were two defensive sectors; Telecommunications Services (+39.36%) and Consumer Staples (+20.22%) as of 27 February 2023.

Higher beta sectors such as Consumer Discretionary, Materials, Real Estate, and Financials lagged behind but still managed to outperform the benchmark CSI 300 Index amid a narrower margin.

But sentiment (technical analysis) suggests that onshore Chinese “A” shares’ outperformance over “H” shares may be limited

Source: TradingView as of 27 Feb 2023

The Hang Seng Stock Connect China AH Premium Index (HSAHP) measures the absolute price premium (or discount) of A shares over H shares for the largest and most liquid mainland China companies with both A-share and H-share listings

In simple terms, when the level of the Index exceeds 100, the A shares are trading at a premium versus the H shares, and when the Index is below 100, the A shares are at a discount versus the H shares.

The major uptrend support of the HSAHP Index in place since the July 2014 low of 88.72 has been broken down since mid-December 2022 which suggests a negative sentiment feedback loop is still in play where the HSAHP Index may continue to trend downwards on a multi-month horizon.

These observations imply that the recent widening of the “AH premium” as seen from its current bounce since late January 2023 may face a headwind near the 142.17 resistance that may see a bearish reversal thereafter.

Hence, given the current rosy expectations on the introduction of more stimulus being priced in ahead of the “Two Sessions” and ignoring other risk factors such as heightened Sino-US geopolitical tension, any “stimulus disappointment” in the coming week is likely to see further softness in onshore China “A” shares; the CSI 300 Index has declined by -18% from its recent medium-term swing high of 4,825 printed on 27 January 2023.

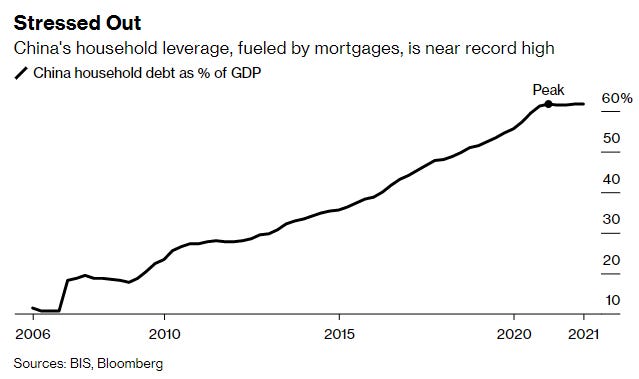

Also, consumers in China are likely to continue to use the extra stimulus packages for advance mortgage prepayments rather than spending or investing in the stock market. In China, over 70% of households own their homes, and close to two-thirds of family wealth is tied to properties.

Household leverage in China has risen steeply over the last ten years and stood near a record high of 61.8% of China’s GDP as of the end of 2021.

If such consumers’ behavior (high propensity for mortgage prepayments) persists, it can further squeeze banks’ net interest margins which are already under pressure from policymakers to provide ample liquidity into the economy via cheap consumer loans. All in all, some form of credit leakages cannot be ruled out.

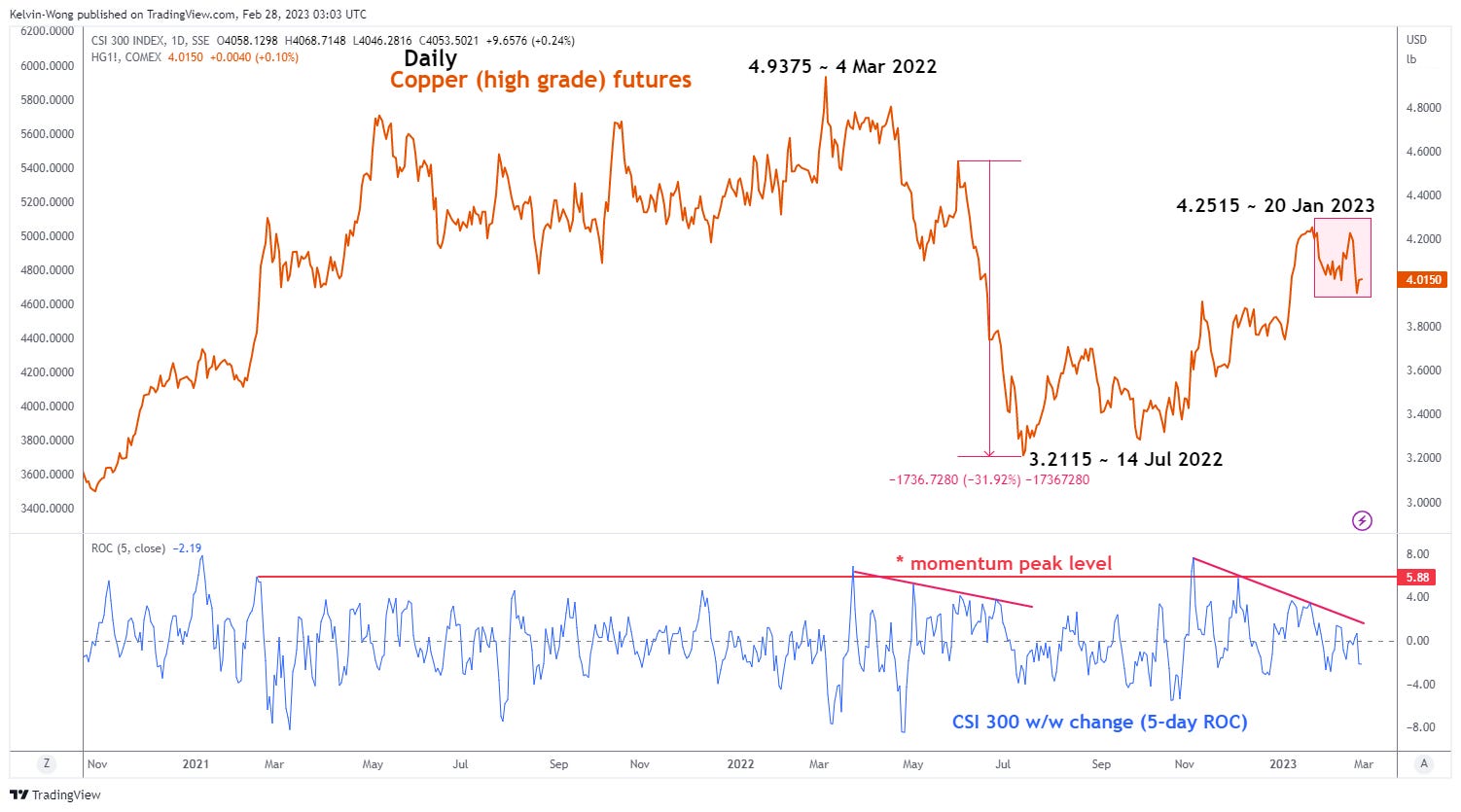

Dr. Copper may soon face a chill from the current softness in China “A” shares

Source: TradingView as of 28 Feb 2023

Given the potential upside limitation of the Hang Seng Stock Connect China AH Premium Index via technical analysis as highlighted earlier, the current softness (momentum) seen in the CSI 300 Index (China “A” shares barometer) is likely to spiral into a negative feedback loop in copper prices.

Based on the 5-day ROC (w/w change) overlayed on the CSI 300, it has reached a key momentum peal level of 5.88 coupled with a bearish divergence signal, and such similar observation in the period of 5 May 2022 to 6 June 2022 has led to 32% decline in the prices of Copper (high grade) futures.

Perhaps, Dr. Copper may soon enter into a medium-term “winter season”

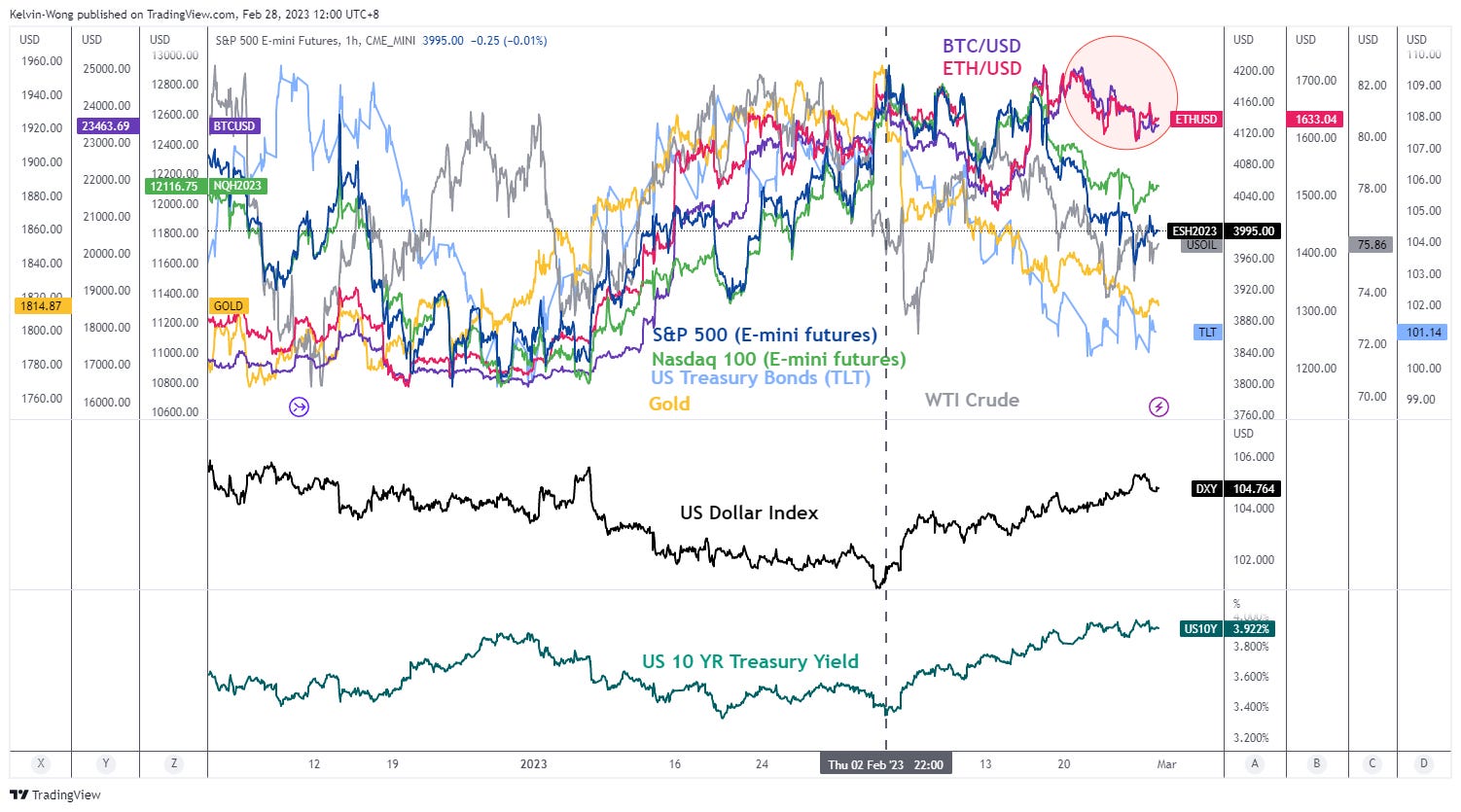

After 2 weeks of upward grinding, cryptocurrencies have now started to feel the chill from rising bond yields

Source: TradingView as of 28 Feb 2023

Cryptocurrencies’ role as a risk diversifier is still in limbo as the magnificent run-up in the majors; Bitcoin and Ethereum since the start of the year have started to see their respective upside momentum dissipating in line with the recent softness seen in US equities, WTI crude oil and gold in the backdrop of rising bond yields.

Source: TradingView as of 28 Feb 2023

Integrated technical analysis suggests that Bitcoin (BTC/USD) may see a medium-term decline below 25,365 key medium-term pivotal resistance towards the 19,910/18,150 support zone which also confluences with the 200-day moving average and the former descending channel resistance from its November 2021 all-time high swing high; a risk of -15%/-22% decline from the current level.

Global Macro Charts Of The Week – curated based on integrated technical analysis (fractals, momentum & graphical)

New additions…

FTSE China A50 Index futures (CN-SGX) – Evolving within a short-term downtrend

Source: TradingView as of 28 Feb 2023

Key technical elements are now advocating for further potential weakness for the FTSE China A50 Index futures.

There are still no clear signals to indicate that the short-term downtrend in place since its 27 January 2023 high of 14,445 high is over. Watch the 13,820 key medium-term pivotal resistance for a further potential down move toward the supports of 12,780 and 12,415.

However, a breakout with a 4-hour close above 13,820 invalidates the bearish scenario for a squeeze up to retest the recent medium-term swing high at 14,410.

Copper high-grade futures (HG-COMEX) – At the risk of a short-term bearish reversal

Source: TradingView as of 28 Feb 2023

The recent medium-term uptrend phase of Copper (high-grade) futures in place 15 July 2022 low of 3.1315 has started to exhibit signs of exhaustion. Watch the 4.1105 key medium-term pivotal resistance (also the former ascending support from the 19 October 2022 low) for a potential slide toward 3.7425 and a break below it exposes 3.5780 next.

On the other hand, a breakout with a 4-hour close above 4.1105 invalidates the bearish scenario for a push-up to retest the 18 January 2023 swing high of 4.3550 in the first step.

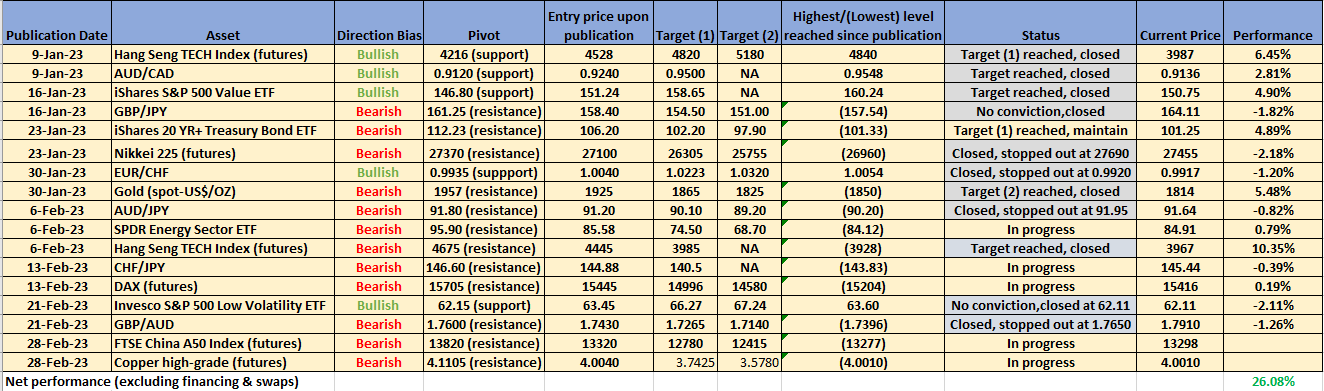

Short-term Tactical Global Macro Model Portfolio

Below is a summary table of assets from prior newsletters’ “Global Macro Charts Of The Week”

Source: TradingView as of 28 Feb 2023

Disclaimer

The content of this newsletter should not be construed as a solicitation to invest and/or trade. This is not trading/investment advice and all content is portrayed as opinion. Past performance is not indicative of future performance.

That’s all for today. I hope you enjoyed my analyses; do feel free to forward them to your friends, and colleagues. Remember to subscribe to the newsletter for the latest updates.

Love the work! Thanks for sharing :)